financial advice. You should do your own research before making any decisions.

Fed Dilemma & Bitcoin as a Neutral Reserve Asset

Takeaways from their discussion, below. Luke Groman believes:

- The dollar will continue in its current status as a reserve currency for the next 10-20 years.

- But, treasury bonds are unlikely to be the primary reserve asset for the next 10-20 years. Some sort of neutral reserve asset has to take treasury bonds' place, and this is already happening with central banks buying gold.

- CPI will be in the double digits within the next few years.

- Bullish bitcoin price action in the next few years - Luke has ~10% of his liquid net worth in bitcoin.

- “Tail risk” that governments could “shut down the on/off-ramps for Bitcoin” for an unspecified period, similar to how gold was illegal to own in the US.

Partial transcript of the interview follows:

[…]

19:13 Natalie: Well can you crystallize that a little bit more just in terms of where you see the dollar going in the next 10-20 years? Being that it is the reserve currency right now and that a lot my listeners who are big proponents of bitcoin see that as potentially nations moving toward a global neutral reserve currency. But at the same time, China has its own CBDC, Russia has come out against Bitcoin and then they teetered back and forth. They have said at one point that they perhaps might even accept oil payments in Bitcoin. So I think we’re a little bit all over the place, but, 10-20 years out is the dollar still the global reserve currency?

19:53 Luke: I think you have to separate into reserve currency and primary reserve asset. I think the dollar will still be a reserve currency if not the primary reserve currency.

20:05 Natalie: As a payment rail.

20:07 Luke: As a payment rail, right.

20:09 Natalie: Okay.

20:09 Luke: In the way that English is still the primary spoken language, there’s a network effect, etc. I think there’s very little chance that the treasury bond is still the primary reserve asset in 10 years or 20 years. And I think some sort of neutral reserve asset has to take its place, will take its place, is taking its place. I mean, de facto, its already happening.

20:27 Natalie: Gold.

20:27 Luke: Gold, if you look at the last nine years, global central banks have net sold \$60 billion in treasures and they’ve bought over a quarter trillion dollars worth of gold. And people say, so what, its only a quarter trillion dollars. And you say, so what, until they revalue it, because central banks have a printing press and they can revalue it whenever they want. In theory, you can turn \$250 billion into \$2.5 trillion in a big hurry, for example. So its just a matter of enough central banks getting together and revaluing it with a couple oil producers.

21:03 Luke: So, I think the dollar’s reserve status will continue. I think the treasury’s primary reserve status is already on the way out, out of necessity. Some of this is driven by a desire to hurt elements in Washington. But I think it is more out of weakness really that China is pushing this, that Russia is pushing this. They have to, because Russia can’t keep selling oil that goes up 8% a year, for treasuries. You actually hear it in Putin’s speech in June, said FX reserves decline at 8% per year. Where’d he get that number from? US federal debt has grown 8% CAGR, every year. And I tweeted about this last year. I said, look, if you think this is a good deal, that Russia takes treasuries as payment, as settlement payment for oil, when the debt is growing 8% and the coupon on the treasuries hasn’t been over 2% in forever. Call me, I’ll borrow a billion from you. I’ll borrow 8% more from you at 2%. And people are like, how are you gonna pay me back? Its a Ponzi. I’ll pay you back out of what you give me next year, and then I’ll keep the difference, and I’ll just keep doing it.

22:18 Natalie: Yea.

22:19 Luke: So, there is this primary reserve asset, primary reserve currency, I think the dollar is fine. I think the reserve asset is on the way out already. You’re seeing this system shift. Its out of necessity from nations like Russia and China in particular… Now, what does the dollar do? What does that mean for the dollar? Here, too, I think there’s two things. With what is happening right now, its really a binary thing. Is the Fed monetizing enough US deficits, or are they not? When they aren’t, the dollar is gonna go up. And the dollar’s gonna go up, and its gonna go up until stuff breaks. And then it will go up even faster. And in theory, the dollar could be at $500 on the DXY and we’ll all be standing in line at a gas station wondering why our dollars don’t buy any gasoline, why there’s no gasoline in the pumps. That’s sort of the natural terminus of all this because it will break global supply chains. So, as long as the Fed is not buying enough treasuries and monetizing enough debt, the dollar is going to go up. Ultimately, the government is very short dollars so they have to eventually come in and monetize that and that’s where we get, to your point, where we are now. Which is, you’re seeing strains in the system, you’re seeing the economy weakening, its very weak elsewhere, but inflation is still elevated. And this is just a classic emerging market problem, which is, listen, if they really want to stop inflation, they do have to break everything. But with debt where it is, you’re gonna be talking about sovereigns defaulting on their debt. They can’t afford that either. So, you’re seeing governments and central banks stuck between a rock and a hard place in a way that I don’t think they’ve seen since the aftermath of World War 1. And at a scale, that as far as I’m aware of, has never happened before, in terms of the amount of debt and the amount of derivatives, and so forth.

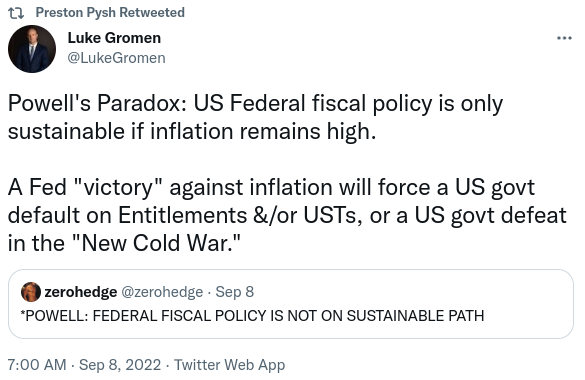

24:15 Natalie: Well, I mean, that kind of speaks to your recent tweet, you said Powel’s paradox: US Federal fiscal policy is only sustainable if inflation remains high, a Fed victory against inflation will force a US government default on entitlements and our US treasuries, or a US government defeat in the new Cold War. Do you want to expand on that a bit?

24:33 Luke: Yea, its really straightforward. Reinhart and Rogoff, who are two of the foremost experts on global sovereign debt and global sovereign debt bubbles. Reinhart I believe is now the president of the world bank, Rogoff was the chief economist at the IMF. They highlighted that, and this is via Hershman Capital, that over the last 220 years, every nation that hit 130% debt to GDP, 98% of them defaulted on their debt, almost all of them via a sustained period of high inflation to basically increase GDP nominally, decrease debt, basically bond holders lost. We saw this in the United States after World War 2, where debt to GDP was 110%. We saw US real interest rates go to -14%, so inflation was 16%, the Fed capped yields at 2%, and bond holders lost money on a real basis. Debt to GDP went from 110% to 55% in just 5 years. Thank you for your donation treasury holders, US is back on its feet, and away we go, right?

25:40 Natalie: Uh-huh.

25:41 Luke: And this has happened over and over and over. Now, there were a few hyperinflations and there were a few restructurings, nominal defaults, but that’s not likely what’s gonna happen. So, you can go back to 2021 where we saw nominal GDP ran 11.5%, CPI ran 8%, and debt to GDP in the United States went from 129% to 122%. We de-levered. At the time, I thought they were gonna continue to do that. They literally laid that playbook out in August of 2019. Stan Fischer, two other former central bankers, said hey, in the next crisis, we’re going to have to cap yields, print money, inflate away the debt. So far so good. Politically, inflation began to be a problem. Our view all a long has been that you’ve gotta inflate the debt to GDP back to 70-80% in the United States or else if you try to tighten beforehand its gonna be a disaster. And, politics being politics, in an election year, they tried tightening beforehand. Fast forward 8 months, we’ve got 60-40 portfolio, you know 60% stocks 40% bonds, it is a disaster. It is the worst year in 50 years of data, data going back 50 years. Worst year for the 60-40 portfolio. The economy is soft, et cetera. So you’ve seen it not working. Where we get to with that tweet specifically is, if you look at, and the reason why I thought it would be a disaster if they tried to tighten too soon, was if you look at what we call the government’s big three expenditures: its treasury spending, its entitlements, its defense. Those three were, after COVID, 140% of tax receipts. Even with the inflation and nominal GDP growth we saw in 2021, it took that 11% nominal GDP growth and 8% CPI to get what we call true interest expense, which is just entitlement pay-goes, plus treasury spending, below tax receipts. So basically you were seeing the US’s effective interest expense above tax receipts until they inflate it the way they did. They got it back below. Great, keep doing it. Then you stop, reverse course. So, the point of that tweet is that Powel needs this inflation. He needs to get this true interest expense further back below tax receipts, so that basically the US government isn’t crowding out global dollar markets, sending the dollar higher and higher and breaking things, for lack of a better word. But that’s not what they’re doing, they’re doing the exact opposite.

28:33 Natalie: Well, I heard you say on a recent podcast that you expect next year’s inflation rates to be in the double digits. So, how do we get there, and what does that mean for everything from equities, to the housing market, to bitcoin, and bonds?

28:48 Luke: I think we’re going to see, I think we’ve seen the local high, I think the local high in CPI was July, whatever that print was, 9, or whatever. But I think people are going to be surprised how quickly things unhinged between what the Fed has already done, but more importantly, what we’re seeing in energy in Europe, in Japan. I think we’re going to see the global economy really come unhinged, and when that happens, and I think its a when and I think its pretty soon, the Fed is gonna be forced to reverse course, to preserve the system, that basically, their choice is going to be, either stand aside and let the whole thing burn to the ground, or…

29:31 Natalie: Deflationary bust, on a grand scale, yea.

29:34 Luke: On a grand scale, on a grand scale. Up to and including western sovereigns defaulting on their debt. And yes, the United States would go last, but it would go if the Fed doesn’t get in there. So then, you’re going to be faced with a situation where the Fed’s gonna have to stop with QT, stop with the interest rate hikes, cut interest rates, start regrowing their balance sheet, with CPI still probably 4, 5, 6? And that’s why I think its very possible, if not likely, that we’ll see CPI back into the double digits, because its just, they didn’t let debt to GDP go far enough down, get inflated away enough, to not create a disaster. And this is before all the geopolitical stuff. It was gonna be a disaster no matter what, Putin just threw a spanner in the works with what’s happened and then the reactions to all these things.

[…]

31:21 Luke: …ultimately, its about that nominal GDP relative to the interest rate and what the government’s paying to get that debt to GPD number down…its going to be challenging, because the discrepancies are going to have to be so big now because could have done this, should have done this, 10 years ago, 12 years ago, they didn’t. Its this dogmatic religion about preserving the real value of the bond market, and now, the numbers are just so big. You’re going to have to run negative real rates 10% for 3, 4, 5 years to get debt to GDP to sustainable levels from which you can normalize policy.

32:07 Natalie: Well, so, do you see this playing out basically as a major capitulation event, and we have a true bottom, not like the one we saw back in June, and then the money printer goes brrrr, and suddenly we see equities rallying again, you know, some of the growth stocks, not just commodities, rallying, and bitcoin potentially going back? How do you actually see this playing out?

32:30 Luke: I’ll put an asterisk here that I’m free to change my mind, the Druckenmiller caveat. The way I think it’s going to play out is, I think we’re going to see the Fed do another 75 basis points this week, the market will tremor a little bit on that. I understand were from an oversold position now, whatever. I think our policymakers and investors are wildly underestimating how bad what has already happened in Europe is going to impact the economy and then how that is going to ripple through highly-levelered economies, highly-levered markets. And so I think you’re going to get a whoosh down sometime over the next 3, 4 months, and at that whoosh down, its not just gonna be markets, its going to be economies whooshing down. And I think you’ll see strains that central bankers simply won’t be able to ignore. Stock market goes down, they don’t care. You even saw today, biggest tail on a 10-year treasury auction, 3 basis points, biggest tail in 10 years. What happens when that’s a 5 basis point tail, 8 basis point tail, 10 basis point tail. These are the types of things where they’ll have to go, okay, and they’ll come in with its treasury market functioning, its not QE, we’re not growing our balance sheet for QE, we’re growing it for treasury market functioning. And, you know, don’t worry, its not inflationary, its just treasury market functioning. And of course it’ll be inflationary. Of course its QE, just like it was in 4Q19, when it wasn’t QE. And I think it’ll almost be like a, I think how it’ll play out will almost be a version of what we saw in COVID on steroids, which is a whoosh down, and then a whoosh up, but I think on the whoosh up, its going to whoosh for a lot longer, because ultimately the bond market will go, wait a second, I think this is the last iteration where they can trick the bond market into believing that this isn’t, sort of, permanent. So I think it’ll be a really interesting time because I think you’ll see assets, growth stocks, commodities, yes, and yes. For my entire career you’ve had the 60-40 portfolio, right, which has been 60 percent stocks, 40 percent bonds. And the 40 percent bonds is always the ballast, and the 60 switches back and forth: growth, value, growth, value. I think this next iteration will be 60 percent growth, 40 percent value, or vice versa. And the bond market will go, oh my god, this is never stopping, just get me out of bonds. And so that’s why I think the whoosh on the other side, or the take-off on the other side, will be epic, because that bond market’s gonna be selling itself to the Fed. I think that will force them into some version of yield-curve control. So it’ll be we’re doing treasury functioning management, this is not QE, and then, as yields keep moving up or testing them, this is yield management, but its not yield curve control, they do not want to say that, because for them, yield curve control for the Fed in particular, is Hotel California. That is, the Fed is going to buy every bond out there, their balance sheet goes 9 trillion, 12 trillion, 20 trillion, 30 trillion, pretty quickly. So, that’s how I think its going to play out, is, I think we’re going to get this risk off driven by what’s already happening in Fed tightening, geopolitically, energy problems, and then I think that will show up in currency markets or sovereign debt markets, somewhere. Here, Japan, Europe, I don’t know. China even, maybe. I don’t know. But once that happens in the West, it starts to go, game on, where they have to go in to address these issues in sovereign debt markets, and once that happens, here we go.

36:57 Natalie: Yea, off to the races, I mean, when you say all this its fascinating. And all I’m thinking in the back of my head is bitcoin, bitcoin, bitcoin, will probably be the beneficiary of that as well.

37:04 Luke: Yes, I agree.

[…]

Topical recent tweets from @LukeGromen